Best Medical Insurance Companies in Kenya (2026): The Policy Gaps Most Buyers Miss

You asked whether maternity was covered. The answer was yes. You booked your preferred consultant at Aga Khan and expected your medical cover to carry the main cost.

The delivery bill was KES 290,000.

Your maternity sublimit was KES 200,000.

The remaining KES 90,000 was yours to pay — not because the policy failed, but because it worked exactly as written. “Covered” did not mean fully paid.

That is the problem with comparing medical insurance in Kenya by insurer name, premium, and headline inpatient limit. A policy can look strong on paper and still leave you exposed at the exact moment you need it.

That is why any serious search for the best medical insurance companies in Kenya should start with fit, not ranking.

Best for which hospital? Best for which family stage? Best for which claim scenario? Best under which waiting period?

This guide compares nine actual medical insurance schedules in Kenya to show where the gaps sit, what each option is best suited for, and what to confirm before you sign.

At Amssurity Insurance, we treat “best” as a policy-fit question, because the best cover is not the one that looks strongest in a brochure. It is the one that still makes sense when your family needs to claim.

For the broader foundation on how medical cover works, start with our guide to health insurance in Kenya, then return here for the policy-level details most buyers miss

Table of Contents

What this guide is really comparing

This guide does not rank the best medical insurance companies in Kenya by name recognition, brochure promises, or the biggest headline inpatient limit.

It compares selected medical insurance options by the gaps that usually matter at claim time:

- Maternity sublimits

- Cancer ceilings

- Hospital copayments

- Outpatient depth

- Waiting periods

- Exclusions

- Claim-time fit

The question is not:

Which is the best among the best medical insurance companies in Kenya?

The better question is:

Which policy is least likely to fail your household when maternity, cancer treatment, outpatient care, copayments, or waiting periods are actually tested?

That is the lens we use in this guide.

What changed in medical insurance in Kenya in 2026

By 2026, comparing medical insurance in Kenya is no longer just about finding the biggest inpatient limit.

The real question is what that limit does after SHA/SHIF coordination, private hospital costs, sublimits, copayments, waiting periods, and international cover rules are applied.

The old shortcut was simple:

Compare insurer, premium, and inpatient limit.

That shortcut is now risky.

1. SHA/SHIF changed the claims environment

Buyer risk:

Your private medical cover may not respond exactly the way buyers were used to under the old NHIF-era assumptions. Depending on the insurer, benefit category, and claim process, some claims may involve SHA/SHIF coordination, statutory rebates, or additional documentation.

Ask before buying or renewing:

- Is the claim settled gross or net of SHA/SHIF rebate?

- Does pre-authorisation require SHA/SHIF participation first?

- Which benefits are affected?

2. Private hospital costs kept rising

Buyer risk:

A policy that looked adequate last year may now carry yesterday’s numbers. This matters most for maternity, surgery, cancer treatment, diagnostics, specialist outpatient care, and premium private hospitals.

Ask before buying or renewing:

- What is the current billing estimate from your preferred hospital?

- Does your maternity sublimit still match that estimate?

- Will your cancer ceiling survive a serious treatment phase?

- Will your outpatient limit survive normal family usage?

- What copay applies at your preferred hospital?

3. International cover became part of the local decision

Buyer risk:

International private medical insurance may now be part of the Kenya advisory conversation, but it should not be treated as a direct substitute for local family medical insurance. Local and international covers solve different problems.

Ask before buying or renewing:

- Are you buying local cover, international cover, or do you need both?

- Where will treatment most likely happen?

- Is evacuation included?

- Can you access outpatient care locally?

- Who handles claims administration?

- What exclusions apply?

The practical implication

Medical insurance in Kenya should no longer be compared by headline inpatient limit alone.

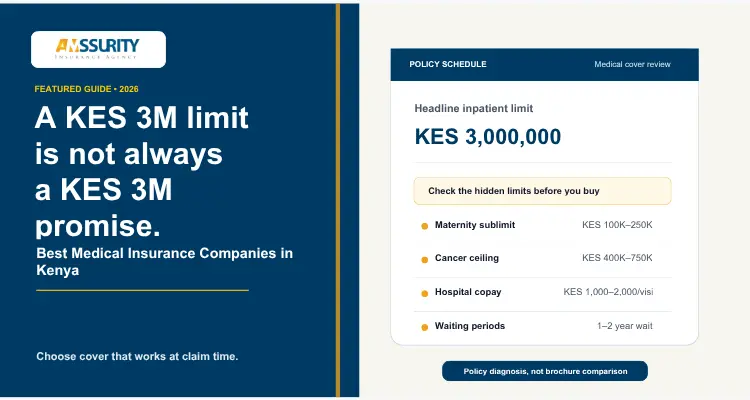

A KES 3M or KES 5M inpatient limit may still behave like a much smaller policy if the claim falls under a low maternity sublimit, a restricted cancer ceiling, a thin outpatient benefit, a premium hospital copay, a waiting period, or a SHA/SHIF coordination rule the buyer did not understand.

The better question is not:

Which insurer is most popular?

Or even:

Should I buy local or international cover?

The better question is:

Which structure matches where my family lives, where we seek treatment, and where the claim is most likely to happen?

Quick guide: Which buyer situation are you in?

Two families can buy medical cover from the same insurer and still need completely different protection.

A family planning maternity, a household with young children, a person managing a chronic condition, and someone living or working across borders are not buying the same kind of medical insurance — even when the insurer name is identical.

Use this table before comparing premiums or inpatient limits.

This is why “best medical insurance company in Kenya” is the wrong starting point. The right starting point is the claim scenario your household is most likely to face.

The mistake most buyers make when comparing medical insurance

Most Nairobi professionals searching for the best medical insurance companies in Kenya compare three things: the insurer’s name, the annual premium, and the headline inpatient limit.

That looks like due diligence. It can still leave you exposed.

What most buyers compare — and what it cannot tell you.

| What buyers compare | What it cannot tell you | Claim-time risk |

|---|---|---|

| Insurer name | Whether the policy fits your hospital, family stage, or likely claim scenario | You choose a familiar brand but miss the benefit structure |

| Annual premium | Whether the cheaper plan has weaker sublimits, waiting periods, or copayments | You save on premium but pay more during treatment |

| Headline inpatient limit | Whether maternity, cancer, outpatient care, and chronic conditions sit under smaller limits | A KES 3M limit behaves like a much smaller policy |

The comparison that matters is not premium versus premium. It is benefit structure versus your actual risk profile.

Name, premium, and headline limit cannot tell you whether your maternity sublimit covers delivery at your actual target hospital.

They cannot tell you whether a KES 3M inpatient limit hides a KES 400,000 cancer ceiling inside it.

They cannot tell you whether your preferred hospital costs you KES 1,000 or KES 2,000 every time you walk through the outpatient door.

The best medical insurance companies in Kenya are not the best in the abstract. They are best for your specific situation: your hospital, your family stage, your likely medical events, and the policy wording that applies when you claim.

Four medical insurance details that decide what your family pays at claim time

1. Maternity sublimit vs. your actual hospital

The hidden issue

“Maternity included” is not the same as “maternity sufficient.”

This is one of the most misunderstood parts of maternity cover in Kenya because buyers hear “maternity included” and assume the benefit matches the hospital they intend to use.

Why it matters

The reviewed schedules include maternity benefits either as inbuilt benefits or optional add-ons.

A normal delivery at Aga Khan starts at KES 200,000. A C-section runs from KES 350,000 to KES 600,000 or above. Eight schedules can produce eight different out-of-pocket outcomes.

Check before buying

Before you buy on the basis of “maternity included”:

- Get the exact maternity sublimit in writing.

- Separate the emergency C-section limit from the general maternity limit.

- Confirm whether normal delivery, elective C-section, and emergency C-section are treated differently.

- Hold the limits against a billing estimate from your preferred hospital.

Advisory note: The headline inpatient limit may not govern the maternity claim.

2. The cancer sublimit inside your inpatient limit

The hidden issue

This is the one most professionals never see until the claim.

In most of the reviewed schedules, cancer treatment is governed by the pre-existing/chronic conditions section rather than a standalone cancer line.

Why it matters

Cancer cover in Kenya should not be checked by looking only at the inpatient limit. You need to find:

- The actual cancer ceiling

- The waiting period

- Whether treatment sits under a dedicated benefit

- Whether it shares a chronic/pre-existing sublimit

Heritage HeriAfya is the exception in this review. It lists cancer as its own separate benefit with its own specific sublimit at each plan tier.

Every other insurer in this review requires you to find the cancer ceiling by reading the pre-existing/chronic conditions section — a clause most buyers never open.

Check before buying

Search the policy schedule for the word “cancer.”

If you cannot find a dedicated cancer line, check the pre-existing and chronic conditions section.

Advisory note: Do not assume that a high inpatient limit automatically means a high cancer benefit.

3. The hospital copayment hiding inside your premium

The hidden issue

You chose Aga Khan. You are on your insurer’s panel. You still pay every time you walk in.

Most major insurers apply outpatient copayments at premium private hospitals. The amounts vary, and the differences matter for a family making frequent specialist visits.

Why it matters

Medical insurance copayments are not always obvious when you compare premiums, but they affect the real cost of using your cover at premium hospitals.

What you pay per visit at Aga Khan and Nairobi Hospital — by insurer.

| Insurer | Aga Khan / premium hospital outpatient copay |

|---|---|

| Old Mutual Afyaimara | KES 2,000 per visit |

| APA Jamii Plus | KES 1,500 per visit |

| Heritage HeriAfya | KES 1,000 per visit |

| AAR | KES 1,000 per visit |

| Fidelity | KES 1,000 per visit |

| Jubilee | KES 2,000 per visit |

| Britam | KES 1,500 per visit |

| CIC | KES 2,000 per visit |

| Madison | KES 1,000 per visit |

Copayment figures are indicative and subject to change at renewal. Verify the exact figure on your policy schedule before your next visit — not after.

Five specialist visits per year at Old Mutual, CIC, and Jubilee costs KES 10,000 in copayments alone, before a single treatment is billed.

Check before buying

This is not necessarily a dealbreaker. It is a cost that belongs in your calculation before you sign.

Ask:

- What is the copay at my preferred hospital?

- Is it per visit, per claim, or per service?

- Does it apply to outpatient only or to other benefits too?

- How many outpatient visits does my household realistically make in a year?

4. Outpatient depth vs. your family’s real usage

The hidden issue

The outpatient limit is where many families discover whether their policy fits daily life, not just emergencies.

A specialist consultation at Aga Khan runs KES 4,000–8,000. A diagnostic episode runs KES 15,000–30,000.

A family with two young children can exhaust a KES 50,000 outpatient limit before the year reaches August.

Why it matters

The difference between a KES 50,000 and KES 150,000 outpatient limit feels theoretical when you are buying. It becomes concrete by July.

One structural note from the reviewed schedules: AAR covers chemotherapy and radiotherapy under the outpatient benefit. Most chemotherapy in Kenya is administered as outpatient infusions. On AAR’s Platinum plan, the outpatient limit is KES 250,000 per person.

Whether this is an advantage or a constraint depends entirely on your plan tier and how you expect to use it.

Check before buying

Before choosing a plan, estimate your household’s real outpatient usage:

- Paediatric visits

- Specialist consultations

- Repeat diagnostics

- Chronic medication reviews

- Dental and optical use, where applicable

- Preferred hospital copays

Advisory note: A low outpatient limit may still work for a low-usage household. It is a poor fit for a family using premium private hospitals frequently.

Medical insurance companies in Kenya compared: where selected plans differ at claim time

The plans below sit broadly within the KES 2M–3M inpatient range, but they do not behave the same way at claim time.

A similar inpatient limit can produce very different outcomes once maternity sublimits, cancer waiting periods, cancer ceilings, and premium-hospital copayments are applied.

Figures are taken from insurer benefit schedules, policy brochures, hospital billing estimates where available, and Amssurity’s advisory review process. Benefits, copayments, panel access, and underwriting rules change, so always confirm the current schedule before buying or renewing cover.

Maternity cover, cancer limits, and copayments — side by side.

| Insurer / plan reviewed | Maternity limit / position | Cancer wait | Cancer ceiling | Aga Khan outpatient copay |

|---|---|---|---|---|

| Jubilee J-Care — Advanced, 2M | KES 120K, optional add-on | 2 years | KES 400K, pre-existing sublimit | KES 2,000 per visit |

| APA Jamii Plus — 2M plan | KES 250K max, optional add-on | 12 months | KES 500K, pre-existing sublimit | KES 1,500 per visit |

| AAR — Silver, ~2M | Inbuilt; 1-year wait | N/A — outpatient | Within outpatient limit | KES 1,000 per visit |

| Old Mutual AfyaImara — Option III, 3M | KES 100K, inbuilt | 12 months | KES 700K, pre-existing sublimit | KES 2,000 per visit |

| Britam Milele — Silver | KES 220K, standalone, 10-month wait | 12 months | KES 800K, pre-existing sublimit | KES 1,500 per visit |

| CIC Family Medisure — Superior, 2M | KES 100K, inbuilt | 12 months | KES 500K, shared sublimit | KES 2,000 per visit |

| Heritage HeriAfya — 2M plan | KES 200K max, optional add-on, 8 tiers available | 2 years | KES 750K, separate cancer sublimit | KES 1,000 per visit |

| Fidelity My Afya Shield — Plan C, 2M | KES 100K, optional add-on | 2 years | KES 400K, pre-existing sublimit | KES 1,000 per visit |

| Madison BetterLife Premier — Option III, 3M | KES 200K, inbuilt | 1 year | KES 700K, shared sublimit | KES 1,000 per visit |

Figures are drawn from policy schedules and product guides current at the time of review. Sublimits, waiting periods, and copayments change at renewal — always verify against your specific policy document before making a claim decision.

How to read this table

Do not use this table to pick a winner. Use it to spot the pressure points.

If you are planning maternity, the maternity sublimit and C-section wording matter more than the insurer name.

If cancer protection is a concern, check whether the cancer benefit has its own ceiling or sits inside a chronic/pre-existing sublimit.

If you use premium private hospitals, the outpatient copay changes the real cost of your cover.

If a column says “confirm current schedule,” do not treat the gap as harmless. Treat it as a question that must be answered before you buy or renew.

The table is not the final answer. It is the shortlist of questions to resolve before you buy, renew, upgrade, or switch.

Medical insurance companies in Kenya reviewed: what each plan is best suited for

The reviews below are not rankings. They are claim-time fit notes based on the selected schedules reviewed.

A plan that works well for outpatient-heavy families may be weaker for maternity. A plan with clear cancer wording may still carry a long waiting period. A plan with a familiar insurer name may still need closer review if your family uses premium private hospitals.

Use each review to identify the trade-off, not to crown a universal winner.

Jubilee J-Care medical insurance review

Claim-time read:

Jubilee J-Care may suit buyers who value broad access and brand familiarity, but the maternity and cancer limits need careful testing against real claim scenarios.

Best for:

Buyers who want broad hospital panel access and a recognisable claim-payment track record.

The number:

The maternity sublimit on the mid-range Advanced plan is KES 120,000.

A normal delivery at Aga Khan starts at KES 200,000. That leaves a minimum gap of about KES 80,000 before complications, consultant differences, or room-category changes.

Watch for:

Cancer has a 2-year waiting period and draws from the pre-existing/chronic sublimit, which on Advanced is KES 400,000.

Best fit:

Jubilee may fit buyers who prioritise access and insurer familiarity, but it needs careful review for maternity planning and cancer-risk exposure.

APA Jamii Plus medical insurance review

Claim-time read:

APA Jamii Plus may work well for households that want stronger pre-existing condition support and optional maternity flexibility, but the C-section wording needs close attention.

Best for:

A household with pre-existing conditions wanting relatively generous sublimits, or anyone who wants APA’s Femina Plus cancer cash benefit as a separate safety net.

The number:

Maternity is an optional add-on in five tiers. The highest tier is KES 250,000.

The emergency C-section limit is a separate figure: KES 75,000 on the 2M plan and KES 100,000 on the 10M plan.

An emergency C-section at Aga Khan can run above KES 500,000.

Watch for:

The emergency C-section limit and the general maternity limit are not the same thing.

A buyer who reads only the maternity add-on limit and assumes it covers a C-section fully may be exposed.

The Femina Plus cancer payout is also a cash benefit, not a treatment-cost cover. That distinction matters.

Best fit:

APA may suit buyers who want pre-existing condition support, optional maternity tiers, and additional cash-benefit protection, but families planning delivery at premium hospitals should confirm the C-section limits carefully.

AAR medical insurance review

Claim-time read:

AAR is strongest where outpatient depth is the main concern, but it needs closer review where maternity adequacy, inpatient-heavy events, or chronic waiting periods are the buyer’s primary issue.

Best for:

A household where frequent outpatient use is the dominant concern — paediatric consultations, specialist visits, repeat diagnostics, and routine treatment.

The number:

Outpatient limits run from KES 50,000 to KES 250,000 per person.

Chemotherapy and radiotherapy are included within the outpatient benefit.

AAR’s newly diagnosed chronic waiting period is 6 months, compared with 3 months for most other insurers in this review.

Watch for:

If your main concern is a large inpatient event, maternity delivery at a top-tier facility, or fast access for newly diagnosed chronic conditions, the outpatient-first structure needs careful interrogation.

Best fit:

AAR may fit families that use outpatient care frequently and want stronger day-to-day medical support. It may be less straightforward where the primary concern is maternity adequacy, inpatient exposure, or chronic-condition timing.

Old Mutual AfyaImara medical insurance review

Claim-time read:

Old Mutual AfyaImara has a strong critical illness cash benefit and shorter chronic-condition access, but premium hospital users and maternity-planning families need to price the copays and maternity gap carefully.

Best for:

A household that values a shorter wait for newly diagnosed chronic conditions and wants maternity inbuilt rather than purchased separately.

The number:

The Critical Illness lumpsum pays KES 750,000 cash on first diagnosis of cancer, stroke, heart attack, kidney failure, or paralysis.

That is a genuine additional benefit that no other plan in this review matches at this level.

Watch for:

Old Mutual has a KES 2,000 outpatient copay at both Aga Khan and Nairobi Hospital — the highest of any insurer in this review.

Five specialist visits per year equals KES 10,000 in copayments before a single test is billed.

Maternity sublimit on the 3M plan is KES 100,000.

Best fit:

Old Mutual may suit buyers who value the critical illness cash benefit and shorter chronic-condition access. It needs closer review for families planning maternity or using premium private hospitals frequently.

Britam Milele medical insurance review

Claim-time read:

Britam Milele may suit families that want a structured product range and a 12-month cancer waiting period, but the maternity and critical illness waiting periods must be factored into timing.

Best for:

A family that wants a clearly tiered product range, a 12-month cancer waiting period rather than 2 years, and a standalone maternity benefit that scales to KES 250,000 on the Gold plan.

The number:

Cancer falls under the pre-existing/chronic sublimit, but Britam’s 12-month wait is meaningfully better than Jubilee’s, Heritage’s, and Fidelity’s 2-year wait.

On the Gold plan, the pre-existing/chronic ceiling is KES 1,000,000 — the most generous of the mid-tier plans reviewed.

Watch for:

The Critical Illness Cash benefit has a 24-month waiting period.

The maternity standalone benefit requires a 10-month waiting period.

You also need to confirm the overall inpatient plan limit that corresponds to the pre-existing sublimit you need.

Best fit:

Britam may suit buyers who want structured options, better cancer waiting-period positioning than the 2-year alternatives, and scalable maternity support. It is less ideal where maternity or critical illness protection is needed immediately.

CIC Family Medisure medical insurance review

Claim-time read:

CIC Family Medisure may suit buyers who want bundled benefits and inbuilt maternity, but the shared chronic/pre-existing structure needs specific review for households with chronic or cancer-risk exposure.

Best for:

A household that wants maternity inbuilt, cooperative society members who benefit from CIC’s network pricing, or buyers who want the full outpatient panel, including dental and optical, bundled into one product.

The number:

Pre-existing and newly diagnosed chronic conditions share the same sublimit — KES 500,000 on the Superior 2M plan.

That is unusual. Most insurers give newly diagnosed chronic conditions a higher or faster-access limit.

Watch for:

The shared sublimit means your newly diagnosed cancer ceiling and your pre-existing chronic ceiling draw from the same pool.

Maternity is inbuilt, but the sublimit on the Superior plan is KES 100,000.

A normal Aga Khan delivery starts at KES 200,000.

Best fit:

CIC may fit buyers who want bundled benefits, inbuilt maternity, and broad outpatient features. It needs closer review where chronic conditions, cancer exposure, or premium-hospital maternity costs are material concerns.

Heritage HeriAfya medical insurance review

Claim-time read:

Heritage HeriAfya is strong where cancer-benefit clarity matters, but the 2-year cancer waiting period and maternity add-on selection need careful timing.

Best for:

A cancer-risk-aware household that wants to know exactly what the cancer ceiling is, rather than deduce it from a pre-existing conditions clause.

The number:

Heritage is the only insurer in this review that lists cancer as a dedicated benefit with its own sublimit at every plan tier.

On the 2M plan, the cancer sublimit is KES 750,000.

On the 3M plan, it is KES 1,500,000.

Watch for:

The cancer waiting period is 2 years.

Maternity is purchased separately in eight tiers, from KES 50,000 to KES 350,000.

The KES 200,000 maternity option approaches realistic costs for a normal delivery at Aga Khan, but it still leaves limited room for complications, consultant differences, or room-category changes.

Best fit:

Heritage may suit buyers who value clear cancer-benefit wording and dedicated cancer sublimits. It is less straightforward for buyers who need immediate cancer protection or who have not selected the right maternity tier.

Fidelity My Afya Shield medical insurance review

Claim-time read:

Fidelity My Afya Shield may work for cost-aware buyers who value transparent wording, but it is less suitable where higher future limits or stronger cancer protection are central.

Best for:

A cost-aware household that wants explicit disclosure.

Fidelity’s schedule plainly states “Cancer Treatment: Within the pre-existing and chronic sublimit” rather than requiring the buyer to deduce it.

The number:

The maximum plan is Plan E at KES 5,000,000 overall — the lowest ceiling of any insurer in this review.

A buyer who needs KES 7.5M or KES 10M overall cover must look elsewhere.

Watch for:

Cancer carries a 2-year waiting period and draws from the pre-existing sublimit, which on Plan C 2M is KES 400,000.

The 5M cap on the product range limits its appeal for anyone who may need higher cover in the future.

Best fit:

Fidelity may suit buyers who want cost control and clear wording. It needs careful review where cancer protection, higher future limits, or long-term upgrade flexibility are important.

Madison BetterLife medical insurance review

Claim-time read:

Madison BetterLife may fit households that want inbuilt maternity and a shorter cancer waiting period, but the shared sublimit structure needs review where chronic and cancer risks overlap.

Best for:

A household that wants one of the more favourable cancer waiting periods in the market, alongside a useful maternity sublimit built into the plan.

The number:

Madison groups newly diagnosed chronic conditions, pre-existing conditions, cancer, and HIV/AIDS under a single sublimit with a 1-year waiting period, not 2 years.

On the Premier Option III 3M overall plan, that shared ceiling is KES 700,000.

Maternity is inbuilt at KES 200,000 across all three Premier plan options, covering both normal and C-section deliveries.

Watch for:

Cancer, newly diagnosed chronic conditions, and pre-existing conditions all draw from the same pool.

A household managing an existing chronic condition alongside a new cancer diagnosis could exhaust the sublimit faster than expected.

The Budget Plan brings maternity down sharply — KES 75,000 on Option I 1.5M — so plan-tier selection matters significantly.

Best fit:

Madison may suit households that want inbuilt maternity, a shorter cancer waiting period, and a practical mid-tier structure. It needs closer review where chronic-condition costs and cancer exposure may overlap within the same sublimit.

How to use these insurer reviews

Do not read these reviews as a ranking.

Read them as a shortlist of questions:

- Which plan fits your most likely claim scenario?

- Which plan has the gap you are least comfortable carrying?

- Which insurer requires the most clarification before you sign?

- Which policy structure fits your hospital, family stage, and medical history?

The best medical insurance company in Kenya is not the one that looks strongest in a brochure. It is the one whose limits, sublimits, waiting periods, copayments, and exclusions still make sense when your family actually needs to claim.

How to choose the best medical insurance company in Kenya for your family

The wrong question is:

Which insurer is best?

The better question is:

Which policy is least likely to leave my family exposed when the hospital bill arrives?

That shift changes the comparison.

You are not only choosing a brand name. You are choosing how maternity, cancer treatment, outpatient care, copayments, waiting periods, and exclusions will behave when your family actually needs to claim.

Before you buy or renew medical insurance in Kenya, pull out the actual policy schedule and run these five checks.

Step 1: Check the maternity sublimit against your preferred hospital

Find the maternity sublimit in the policy schedule — not the brochure.

Then get a written billing estimate from your preferred hospital for:

- Normal delivery

- Elective C-section

- Emergency C-section

Using Aga Khan as an example:

What delivery actually costs — before your policy is tested.

| Delivery type | Approximate cost range |

|---|---|

| Normal delivery | KES 200,000–350,000 |

| C-section | KES 350,000–600,000+ |

Costs vary by hospital, consultant, and whether complications arise. Verify your maternity sublimit and C-section wording against these figures — not against your headline inpatient limit.

If your maternity sublimit is below KES 250,000, you are likely carrying part of the gap yourself.

Then check separately:

Is there a different emergency C-section limit?

It is often a separate and lower figure.

Buyer protection note: “Maternity included” is not enough. The number has to match the hospital you are likely to use.

Step 2: Find the cancer ceiling, not just the inpatient limit

Search your policy wording for the word “cancer.”

If you cannot find a dedicated cancer line, check the pre-existing and chronic conditions section. In many schedules, that is where the cancer limit sits.

Check:

- The sublimit that governs cancer treatment

- Whether cancer has its own dedicated line

- Whether it shares a chronic/pre-existing sublimit

- Whether the waiting period is 1 year or 2 years

If your cancer ceiling is low, one treatment phase can consume the benefit quickly.

Do not rely on the headline inpatient limit until you have confirmed how cancer is treated in the schedule.

Buyer protection note: A KES 3M inpatient limit does not automatically mean KES 3M for cancer treatment.

Step 3: Price the copayment at your preferred hospital

Find the copayment schedule for your preferred hospital. It is usually in the benefit schedule, provider panel, or general conditions section.

Then estimate your family’s realistic outpatient visits per year.

Most families with young children may make 6–10 outpatient visits annually.

What your copay actually costs over a year of outpatient visits.

| Copay amount | 8 outpatient visits per year |

|---|---|

| KES 1,000 | KES 8,000 |

| KES 2,000 | KES 16,000 |

A KES 1,000 copay difference per visit adds up to KES 8,000 a year for a family that visits the doctor monthly. That figure does not appear on your premium comparison — but it appears on every receipt.

Old Mutual, CIC and Jubilee charge KES 2,000 at Aga Khan. Most others in this review charge KES 1,000. That KES 8,000 annual difference is real money before tests, medication, or specialist procedures are billed.

Buyer protection note: A lower premium can be partly offset by higher usage costs if your family visits premium hospitals often.

Step 4: Run the outpatient reality check

Find your outpatient annual limit.

Then estimate your household’s actual usage.

What outpatient care actually costs — before your limit is tested.

| Service | Approximate private hospital cost |

|---|---|

| Specialist visit at Aga Khan or Nairobi Hospital | KES 4,000–8,000 |

| Diagnostic episode — bloods, imaging, specialist review | KES 15,000–30,000 |

| Realistic annual outpatient use for a family of four with two young children | KES 100,000–150,000 |

A KES 50,000 outpatient limit covers roughly one diagnostic episode and two specialist visits. For a young family, that runs out before the year does. Check the outpatient sublimit on your schedule — not just the inpatient headline.

If your outpatient limit is KES 50,000, it may run out before August.

If you are still working out what premium range makes sense for your household, refer to our breakdown of the true cost of health insurance in Kenya and what different budget levels actually buy.

Buyer protection note: Outpatient cover is where many families discover whether the policy fits daily life, not just emergencies.

If you are still working out what premium range makes sense for your household, our breakdown of the true cost of health insurance in Kenya covers what different budget levels actually buy.

Step 5: Check your medical insurance waiting periods

Medical insurance waiting periods can differ across:

- Pre-existing conditions

- Newly diagnosed chronic conditions

- Maternity

- Cancer

- Dental

- Optical

- Specialist treatment

Do not assume one waiting period applies to everything.

Write down the waiting period for the three categories most relevant to your household.

For example:

Check these waiting periods before you buy — not after you need to claim.

| If your household is focused on… | Waiting periods to check first |

|---|---|

| Maternity planning | Maternity, C-section, newborn cover |

| Chronic condition management | Outpatient, dental, optical, and specialist access |

| Cancer protection | Cancer waiting period, chronic/pre-existing sublimit, critical illness benefit |

| Children’s medical use | Outpatient, dental, optical, specialist access |

Waiting periods are the most common source of claim rejection in the first year of a new policy. Find your household’s row above and check those specific clauses on any schedule you are comparing.

Buyer protection note: The waiting period that matters most is not the general one. It is the one attached to the claim your household is most likely to face.

Final check before you buy or renew

Most Nairobi professionals who run these five checks against their current medical insurance policy find at least one material gap.

Not always a fatal gap. But a gap worth knowing before the hospital asks you to pay it.

The people who find these gaps before a claim are not lucky. They checked while the stakes were still low.

FAQs about the best medical insurance companies in Kenya

The best medical insurance choice is not always the most familiar insurer name. It is the cover that fits your hospital preference, family stage, claim risks, and the trade-offs hidden in the policy schedule.

Which are the best health insurance companies in Kenya?

There is no single best health insurance company in Kenya for everyone.

The better choice depends on your hospital preference, family stage, inpatient limit, outpatient limit, maternity needs, cancer sublimits, waiting periods, copayments, and claims process.

A strong insurer name is useful, but the real question is whether the policy fits your likely claim scenario.

What should I check before buying medical insurance in Kenya?

Before buying medical insurance in Kenya, check the inpatient limit, outpatient limit, maternity sublimit, cancer ceiling, waiting periods, hospital copayments, exclusions, and claims process.

Do not stop at the insurer name or brochure limit. The expensive gaps are usually found in the sublimits, waiting periods, copayments, and benefit wording.

Is maternity cover in Kenya included in all medical insurance plans?

Maternity cover in Kenya is not included in all medical insurance plans in the same way.

Some plans include maternity as an inbuilt benefit. Others offer it as an optional add-on. The key issue is whether the maternity sublimit matches your preferred hospital’s delivery costs.

A policy can say “maternity included” and still leave you paying a large gap if the sublimit is too low.

Does cancer cover in Kenya fall under inpatient insurance?

Sometimes, but not always, as a dedicated cancer benefit.

In many medical insurance schedules, cancer treatment falls under the pre-existing or chronic conditions sublimit. That sublimit may be much lower than the headline inpatient limit.

Always check the actual cancer ceiling, waiting period, and whether cancer has its own dedicated benefit line.

What is the difference between inpatient and outpatient limits?

Inpatient cover applies when you are admitted to the hospital.

Outpatient cover applies when you receive treatment without admission, including consultations, diagnostics, medication, and specialist visits, depending on the policy.

For families with young children, chronic medication needs, or frequent specialist visits, outpatient depth can matter as much as inpatient protection.

What are medical insurance copayments?

A medical insurance copayment is the amount you pay out of pocket when using certain hospitals or services, even when the hospital is on the insurer’s panel.

Copayments are common at premium private hospitals. They should be included in your real cost calculation before you buy or renew medical cover.

A lower premium may not feel cheaper if your family often uses high-copay hospitals.

How do I compare medical insurance companies in Kenya?

Compare medical insurance companies in Kenya by looking beyond the premium and inpatient limit.

Check maternity sublimits, cancer ceilings, outpatient limits, hospital copayments, waiting periods, exclusions, provider access, and claims process.

The best comparison is not between insurers. It is policy structure versus your actual medical risk.

Which medical insurance company is best for families in Kenya?

The best medical insurance company for families in Kenya depends on the family’s stage and hospital usage.

A family planning maternity should prioritise maternity sublimits and C-section wording. A family with young children should check outpatient depth, paediatric access, specialist visits, and hospital copayments.

Family medical insurance should be judged by likely usage, not just the insurer name.

Amssurity advisory note

When comparing medical insurance companies in Kenya, do not stop at the insurer’s name. Compare the limits, sublimits, exclusions, copayments, waiting periods, and claims process against the medical situations your household is most likely to face.

The policy that looks best on paper is not always the one that protects you best at claim time.

Before you renew your medical insurance in Kenya, check the gap first

Most medical insurance gaps do not announce themselves at renewal.

The schedule may look fine. The premium may look reasonable. The insurer name may feel familiar.

But if the maternity sublimit is too low, the cancer ceiling is hidden under a chronic-condition clause, the outpatient limit is thin, or your preferred hospital carries a higher copay, the problem will only become obvious when someone is asking you to pay.

That is why a medical insurance policy review matters before renewal.

It gives you a plain-English view of what to keep, what to question, and what to change — before the decision becomes emotional, urgent, and expensive.

No pressure. No obligation. Just clarity while the stakes are still low.

Medical Cover Review

Before renewal, find the gap your policy will not announce.

Your medical insurance schedule may look fine until maternity, cancer treatment, outpatient use, co-payments, or waiting periods expose a hidden limit.

Our medical insurance policy review in Kenya checks your current cover against your hospital preference, family stage, likely claims, and renewal options — then gives you a plain-English brief showing what to keep, what to question, and what to change.

Your review brief will show:

- What your current medical cover is strong at

- Where the expensive gaps may sit

- What to confirm before renewal or upgrade

- Whether staying, upgrading, or switching makes better sense

No pressure. No obligation. If your current cover is good enough, we will tell you.

The best time to find a medical insurance gap is before the hospital asks you to pay it.

Founder & Insurance Advisor | Amssurity Insurance Agency, an IRA-licensed agency in Nairobi

Agnes Mukulu advises individuals, families, SMEs and diaspora Kenyans on health, motor, business, life and international medical insurance. Having reviewed hundreds of policies, quotations and benefit schedules, she helps clients look beyond premiums to understand benefits, exclusions, waiting periods, excesses and claims requirements. She founded Amssurity to make insurance guidance clearer, more transparent and more practical, helping clients choose suitable cover and understand how it should work when they need it most.