Amssurity shares tips on how to use your insurance, factors to consider when selecting insurance, and also help you benefit from your insurance. We don’t just share information, we educate and empower. Knowledge is power.

There is a dual-income household in Nairobi. Two salaried professionals. One is on an employer group medical scheme. The other is registered under SHA/SHIF and took out a personal top-up three years ago after deciding the employer plan on its own did not feel like enough.

Combined, they are paying roughly KES 180,000 a year in premiums. Assuming that is their total cost of health insurance in Kenya

They have never had a major claim.

They feel covered.

Then one partner is diagnosed with breast cancer. Stage 2. Treatable, with the right care.

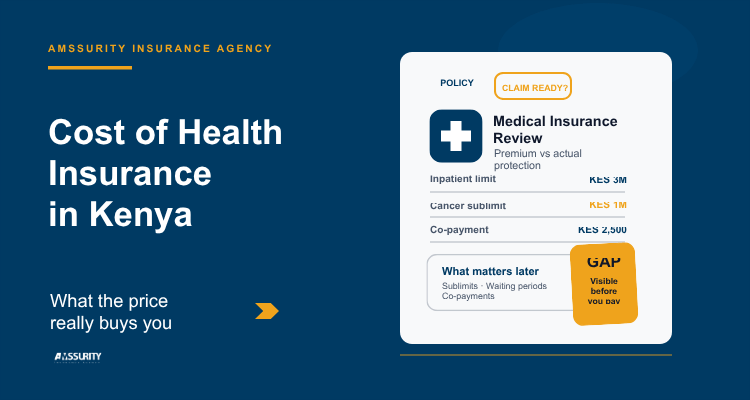

The group scheme has a cancer treatment sub-limit of KES 1.5M. It sounds substantial until oncology costs escalate. In private hospitals like Aga Khan, four cycles of chemotherapy can exceed KES 2M, depending on the drug protocol. If the total bill reaches KES 2.2M, the scheme pays KES 1.5M, leaving a KES 700,000 gap.

The personal top-up has a 24-month waiting period for cancer treatment. The policy is 36 months old, so that part looks fine. But the policy wording defines cancer in a way that excludes malignancies linked to an earlier undeclared investigation. Three years ago, a routine mammogram flagged a benign cyst. It was never followed up. It was never mentioned on the application. At claim time, the insurer classifies that omission as material non-disclosure.

The top-up pays nothing.

SHA/SHIF contributes something, but not enough to close the private-hospital gap.

The household still owes a large amount out of pocket.

They had insurance. They paid every year. They still got a financial shock.

That is the point most people miss when they search for the cost of health insurance in Kenya.

Understanding which policies carry which cancer ceilings — before you need to claim — is exactly what our comparison of the best medical insurance companies in Kenya is built to help you do.

This is not usually a story about careless people. It is usually a story about responsible people who were shown a premium rather than the full trade-off.

The real cost of health insurance in Kenya is not just what leaves your account each year. It is the relationship between three numbers:

What you pay in premiums,

What the policy actually pays when something serious happens,

And the gap you carry yourself if the cover is thinner than it looked at the sale.

That gap is where the most expensive mistakes live.

Run a 10-minute policy review. Send your policy schedule or membership certificate and get a plain-English view of the parts that usually matter most at claim time: sublimits, waiting periods, co-payments, hospital-network issues, and underwriting gaps.

⏱️ 10 min Review🧾 Plain English Read🛟 Claim-time Lens

No obligation. Just clarity. If it will not hold up at claim time, we will tell you.

✔ Specific gaps, not vague advice✔ No obligation✔ Better choices now

What Determines the Cost of Health Insurance in Kenya

When insurers price medical cover, they are answering one question:

How likely are we to pay for this person or family, and how much are we likely to pay?

That is what the cost of health insurance in Kenya is really built on. Not one thing. Several.

1. Age

Age is one of the strongest pricing drivers when it comes to the cost of healthth insurance in Kenya.

It rarely moves in a smooth line. It often moves in bands. That means the price difference between 34 and 35 may be modest, but the difference between 39 and 40 or 44 and 45 can feel sharper than most buyers expect.

That is why delaying entry into a medical scheme is usually expensive twice over: you enter at a higher premium, and you often enter under stricter scrutiny on pre-existing conditions.

Early entry is not just cheaper. It is structurally cleaner.

2. Current health status

This is one of the cost drivers many buyers do not see because it is not always discussed in plain English.

If you are applying for an individual or family policy and you currently have a managed chronic condition, recurring symptoms, ongoing medication, or a recent diagnosis under review, the insurer is not reading that as background information. They are reading it as pricing and acceptance information.

Your current health status can affect the cost of health insurance in Kenya in several ways:

A higher premium,

A waiting period,

A condition-specific exclusion,

A reduced benefit for that condition,

Or, in some cases, a decision not to offer cover on standard terms at all.

This is not punishment. It is underwriting.

The mistake is pretending that current health status does not matter because you feel “basically fine.”

3. Previous medical history

Previous medical history matters even when the issue feels resolved, minor, or old.

A past surgery. A previously managed fibroid issue. A benign cyst. A prior back injury. A long-standing gastrointestinal investigation. A history of high blood pressure that is now controlled. These things still matter because insurers are trying to understand future claims probability, not just your current mood.

This is where many people misunderstand the cost of health insurance in Kenya. They think pricing is about today’s symptoms only. It is not. It is also about the medical story that sits behind you.

That same history also matters later at claim time. If something serious happens and the insurer believes a relevant prior condition or investigation was not disclosed, the argument stops being about premium and starts becoming about validity.

That is a much worse place to discover the gap.

4. Your inpatient limit

This is the figure most people look at first.

It is also the figure most people misread most confidently.

A KES 3M inpatient limit sounds like KES 3M of serious protection. Sometimes it is. Often it is not.

That is because the headline number may sit above a series of smaller numbers:

Cancer treatment sublimit,

ICU sublimit,

Surgical sublimit,

Specialist-fee caps,

Theatre limits,

And condition-specific restrictions.

So when people compare the cost of health insurance in Kenya, they often compare two headline inpatient figures and assume they are comparing the same thing.

They are not.

They may be comparing two very different pieces of protection dressed in similar language.

For a side-by-side comparison of how nine Kenyan insurers actually structure these sublimits — with the specific figures from their policy schedules, read our review of the best medical insurance companies in Kenya.

5. Outpatient cover

Outpatient cover changes the premium materially.

For many households, it is one of the biggest drivers after age, maternity, and underlying health profile.

Whether it is worth it depends on how your family actually uses care.

A family with frequent GP visits, paediatric consultations, prescriptions, and specialist referrals experiences outpatient care very differently from a household that rarely sees a doctor outside emergencies. Hence, its impact on the cost of health insurance in Kenya.

The right question is not “Does outpatient sound useful?”

The right question is: “Based on how we actually use care, does this premium addition reduce enough real out-of-pocket spend to justify itself?”

6. Maternity

Maternity is one of the clearest price drivers in family cover and one of the most misunderstood.

Adding maternity can push premiums up sharply. It also usually comes with a waiting period. So a family planning pregnancy in the next few months cannot just add maternity today and assume the policy will respond tomorrow.

That timing mistake is one of the most common ways people misread the cost of health insurance in Kenya. They think they are buying a benefit. In reality, they may be buying a benefit plus a calendar constraint.

Both matter.

7. Hospital network

Network is not just a convenience choice. It is a treatment-path choice.

If your cover works beautifully at a limited network of mid-tier hospitals but your serious diagnosis leads you toward Nairobi Hospital, Aga Khan, or another top-tier facility, the premium you saved earlier may simply reappear later as a treatment-access problem.

That is why cheaper cover is not always cheaper cover.

Sometimes it is deferred spending disguised as savings.

8. Co-payments and cost-sharing

Co-payments reduce premiums because they push part of the usage risk back to you.

On paper, they often look manageable.

In real life, they accumulate quietly.

A family that makes repeated outpatient visits or uses specialist care regularly can end up paying enough in co-payments over time to neutralise much of the savings that made the policy look attractive in the first place.

That is why the cost of health insurance in Kenya should never be read as premium alone. It must also be read as expected out-of-pocket behaviour.

AMSSURITY INSURANCE AGENCY

Checklist for Health Cover Review

Before you compare prices, check these 7 things first.

Use our 10-minute policy review checklist to spot the gaps most people only discover when they need to claim: sublimits, waiting periods, co-payments, hospital access, disclosure issues, and renewal traps.

📋 7-point Checklist🧠 Self-serve Clarity🚫 No sales pitch First

Useful before renewal, before switching, and before assuming a headline limit tells the whole story.

✔ Practical, not generic✔ Built for real policy checks✔ Low-friction next step

What the Same Premium Range Can Buy You

This is where the conversation gets honest.

Because the real cost of health insurance in Kenya becomes visible only when you stop asking “what is the price?” and start asking “what does that price actually buy?”

Take one profile:

Two adults aged 32–36. Two children under six. No maternity included.

Now compare three policies in a similar general price range.

Compare the real trade-offs

Three policy structures can look close on price and still behave very differently at claim time.

The cheapest premium often buys narrower hospital access, tighter sublimits, or more co-payment friction. Get to know the real cost of health insurance in Kenya.

Read beyond the headline price.

Policy A — Lowest Premium

Best read as the lower-cost option, not automatically the safer one.

Annual premium

~KES 130,000

Inpatient limit

KES 1M

Cancer sublimit

KES 300,000

Outpatient

KES 50,000

Co-payment

SHA rebate per admission, KES 200 – 1,000 per outpatient visit

ICU sublimit

Subject to sub-limit

Hospital access

Mid-tier network only

Policy B — Balanced

A middle-ground option where price and usable benefits are closer together.

Annual premium

~KES 175,000

Inpatient limit

KES 3M

Cancer sublimit

KES 500,000

Outpatient

KES 75,000 annual limit

Co-payment

SHA Rebate per admission, KES 500 – 2,500 per outpatient visit

ICU sublimit

Subject to sub-limit

Hospital access

Mid-tier plus select top-tier

Policy C — Broadest Protection

The higher-limit option where fewer internal restrictions are doing the cost-cutting.

Annual premium

~KES 250,000

Inpatient limit

KES 10M

Cancer sublimit

KES 2,000,000

Outpatient

KES 100,000 annual limit

Co-payment

SHA Rebate per admission, KES 500 – 2,500 per outpatient visit

ICU sublimit

Subject to sub-limit

Hospital access

Full top-tier access

Note: Premiums are illustrative only. Actual pricing varies by insurer, age, family size, hospital choice, underwriting, and benefit structure.

Add maternity, and the price changes again.

Add a chronic condition, a prior surgery, or a more complicated medical history, and the terms may change again.

Same household.

Same intention.

Different underwriting outcome. Different premium. Different claim-time experience.

That is why two families can both say they are paying for medical cover and still be buying completely different levels of actual protection.

Same broad price band. Very different outcome.

The premium tells you what the cover will cost. The details tell you how useful it will be when your family needs care. Use this family medical cover guide to know what to check before choosing.

AMSSURITY INSURANCE AGENCY

Comparison Brief for Families

Not sure which policy is actually better?

Get a Family Quote Pack: 3 matched options plus a plain-English comparison showing the real trade-offs — inpatient strength, cancer and ICU sublimits, waiting periods, co-payments, and hospital-network fit.

📦 3 options Matched🧾 Plain English Comparison🏥 Hospital-fit Focus

Best used after you have already seen the gaps in your current cover.

✔ Trade-offs explained clearly✔ No pressure✔ Better fit, not just cheaper price

What Appears at Claim Time That Nobody Explained Properly at Sale

Sublimits are where “I thought I was covered” often breaks

The policy summary looks simple.

The full schedule usually is not.

Most people do not buy medical insurance by reading forty pages of wording against likely treatment costs at the hospitals they would actually choose. They buy from a brochure, a schedule, a quote comparison, and a conversation.

That is precisely why the sublimit problem keeps recurring.

The headline number creates comfort.

The internal limits create reality.

Before you buy, ask for every meaningful sublimit in writing.

Not because you enjoy paperwork.

Because that is where the difference between premium and protection becomes visible.

Switching insurers can reopen old problems

People assume continuous cover means continuous protection.

Sometimes it does not.

If you move from one insurer to another, you need to ask what happens to waiting periods, previously covered conditions, and any medical history already known under the old scheme.

Do not assume continuity.

Get the answer in writing.

Non-disclosure is where small omissions become expensive

Many serious claim disputes do not begin with fraud. They begin with a sentence like this:

“I did not think that was important.”

That is exactly why previous medical history matters so much in the cost of health insurance in Kenya.

Because what was not priced properly at the beginning may be challenged later when the claim amount is large enough to matter.

If there has been a prior test, prior symptom, prior diagnosis, prior treatment, prior surgery, or a condition you consider minor but memorable, disclose it.

Let the underwriter decide what to do with it.

That is almost always cheaper than discovering at claim time that the silence was more expensive than the premium.

The Questions That Should Come Before the Price Comparison

Before you compare quotes, ask these instead:

Where would I actually want to be treated if something serious happened?

What are the cancer, ICU, surgery, and specialist sublimits in this policy?

How does my current health status affect acceptance, price, exclusions, or waiting periods?

How does my previous medical history affect acceptance, price, exclusions, or future claims?

If I switch from my current scheme, what resets and what carries over?

What out-of-pocket spend will this policy still leave me with in an average year?

These questions are not extra.

They are the real buying process.

Everything else is window dressing.

The Honest Summary

The cost of health insurance in Kenya is not one number.

It is the premium you pay, plus the exclusions and waiting periods attached to your health profile, plus the out-of-pocket risk you still carry, minus the protection that actually shows up when you need to claim.

That is why cheaper is not always cheaper.

And more expensive is not always better.

The right policy is the one where the trade-off is visible before you pay.

You have not misunderstood insurance because you were irresponsible. Most people misunderstand it because the market makes premium easy to see and protection harder to see.

That is the gap Amssurity Insurance exists to close.

AMSSURITY INSURANCE AGENCY

For Protection-Oriented Professionals – Cost of Health Insurance in Kenya

Before you compare prices, find the gaps first.

Run a 10-minute policy review. Send your policy schedule or membership certificate and get a plain-English view of the parts that usually matter most at claim time: sublimits, waiting periods, co-payments, hospital-network issues, and underwriting gaps.

⏱️ 10 min Review🧾 Plain English Read🛟 Claim-time Lens

Founder & Insurance Advisor | Amssurity Insurance Agency, an IRA-licensed agency in Nairobi

Agnes Mukulu advises individuals, families, SMEs and diaspora Kenyans on health, motor, business, life and international medical insurance. Having reviewed hundreds of policies, quotations and benefit schedules, she helps clients look beyond premiums to understand benefits, exclusions, waiting periods, excesses and claims requirements. She founded Amssurity to make insurance guidance clearer, more transparent and more practical, helping clients choose suitable cover and understand how it should work when they need it most.