Affordable Health Insurance in Kenya 2026: What the Premium Hides

The most dangerous word in Kenyan health insurance is “affordable.”

A family of four can buy a Jubilee J-Care Cover Bora for KES 12,600 per year and feel covered. That plan is inpatient-only. Every GP visit, every blood test, every specialist consultation comes out of pocket. For a family with young children, that outpatient gap can easily exceed the annual premium before the policy year ends.

This guide compares eight private health plans with an annual family premium of KES 150,000. For each one, we go beyond the headline limit to the things that only appear at claim time — sublimits, waiting periods, shared limits, and the specific gaps most buyers discover after they need them.

We also cover the SHA/SHIF baseline, what it actually provides in 2026 and where private cover needs to supplement it.

Read the comparison table with that lens.

Table of Contents

Who is this affordable health insurance guide for?

This guide is for you if you are comparing affordable health insurance in Kenya and want to avoid choosing by premium alone.

- You are buying private medical cover for the first time.

- You are a young family comparing inpatient, outpatient, maternity, and paediatric benefits.

- You want a lower-cost plan, but still need realistic hospital access.

- You are comparing SHA/SHIF with private medical insurance and want to know where private cover may still matter.

- You have a chronic condition, planned surgery, or maternity need and want to check waiting periods and sublimits before paying.

The aim is simple: help you see what each affordable plan is likely to do at claim time — not just what it promises in the brochure.

Why “affordable” means more than the lowest premium

Most Kenyan households ask: “How much does medical insurance cost?” and “Which cover is cheapest?”

A cheap plan can become expensive if the outpatient limit runs out, the maternity cap is too low, your hospital attracts a copayment, or a chronic illness claim falls under a smaller sublimit.

In this guide, affordable health insurance means a cover that balances:

- Premium cost

- Inpatient and outpatient limits

- Maternity and chronic illness benefits

- Hospital access and copayments

- Waiting periods and exclusions

SHA provides a national health financing layer, but many families still compare private medical insurance for wider hospital choice, outpatient access, maternity planning, and claim-time flexibility.

This guide compares eight affordable health insurance covers in Kenya and shows what each one offers, where the trade-offs sit, and what to check before buying.

The cheapest cover is only affordable if it still works at claim time.

Kenya’s Social Health Fund (SHA) at a Glance

| Item | 2025 Rule |

|---|---|

| Contribution | 2.75% of gross salary for employees (min KSh 300); means-tested rate for self-employed |

| Penalty | 2% monthly on late remittances |

| Core Benefits | Out- & in-patient, preventive, rehab, palliative care across public Level 4–6 hospitals |

SHA is the baseline affordable health insurance in Kenya because contributions scale with income. Yet cover limits (and queues) often push families toward private plans for faster access or wider hospital panels.

How we selected these affordable health insurance plans in Kenya

We did not rank plans by premium alone. Cheap cover only belongs here if it still gives the buyer useful protection when a real claim happens.

Each plan was checked against five practical tests:

- Premium: broadly affordable for individuals or families.

- Inpatient value: a meaningful hospitalisation limit for the price.

- Hospital access: recognised hospitals and clinics, especially Tier II and Tier III facilities.

- Claim-time clarity: waiting periods, sublimits, copayments, exclusions, and pre-existing condition rules.

- Claims sustainability: insurer claims experience reviewed using IRA data where available.

We treated claims ratios of roughly 65% to 85% as healthier for sustainability. Insurers around 85% to 95% were reviewed more carefully because high claims pressure may lead to stricter renewals, premium corrections, tighter underwriting, or benefit changes.

In short: this is not a list of the cheapest medical insurance plans in Kenya. It is a shortlist of affordable plans that still deserve a serious comparison.

If you are still learning how inpatient cover, outpatient limits, waiting periods, sublimits, and hospital panels work, start with our complete guide to health insurance in Kenya before comparing individual plans.

Affordable health insurance plans in Kenya compared for 2026

This table gives you a quick side-by-side view of the plans, benefits, and key trade-offs to check before choosing.

| Plan | Inpatient | Outpatient | Maternity | Dental / Optical | Claim-time reality |

|---|---|---|---|---|---|

| Madison Betterlife Budget | ✓ | ✓* | ✓* | ✓* | Cancer and chronic illness claims sit under a shared family sublimit of KES 150,000–300,000 — against a headline inpatient figure of up to KES 1.5M. Verify the sublimit on the tier you are buying before paying. |

| Britam Bima ya Mwananchi | ✓ | ✓ | ✓* | ✓* | The KES 75K minimum inpatient is thin for anything beyond a short medical admission. Right as a first cover. Wrong as a plan you expect to carry long-term. |

| Old Mutual Afyaimara County | ✓ | ✓* | ✓* | ✓* | Air evacuation only applies on the 1M inpatient tier. Confirm which tier you are buying before assuming that benefit is included. |

| APA Afya Nafuu | ✓ | ✓* | ✓* | — | No dental or optical at any tier. The strongest outpatient depth in this price range. Right plan if you use outpatient regularly and can absorb dental costs separately. |

| Jubilee J-Care Cover Bora | ✓ | — | ✓* | — | No outpatient cover. Every GP visit, blood test, and specialist consultation is out of pocket. Right plan if you need inpatient protection only and will self-fund all outpatient care. |

| Jubilee J-Care Johari | ✓ | ✓* | ✓* | — | The 200K–400K inpatient ceiling exhausts quickly at a private Nairobi hospital. Best suited to buyers using Tier II facilities, where admission costs are materially lower. |

| CIC Afya Bora | ✓ | ✓* | ✓* | — | Shared limits across the family. Multiple claims in one year — common in a family of six — deplete the pool faster than per-person limits would. The flat KES 32,000 premium is genuine value for a healthy family. Less so for one with chronic conditions. |

| AAR ShwAARi | ✓ | ✓* | ✓* | ✓* | Every outpatient claim reduces what remains for inpatient — they share one pool. On a KES 250K plan, outpatient is capped at KES 75,000 (30%). Once outpatient is exhausted, effective inpatient cover is KES 175,000. Know this before you assume the headline limit applies in full. |

* Available at additional cost. Confirm the exact premium uplift with your broker before purchase.

Quick comparison: best use case and main caution

This quick comparison shows each plan’s strongest use case and the main issue to verify before you buy.

| Claim-time reality | Why it matters | What to ask before buying |

|---|---|---|

| Chronic illness sublimits | Your serious illness cover may be lower than the headline inpatient limit. | What is the chronic, specified illness, and pre-existing condition sublimit? |

| AAR shared pool structure | AAR may avoid a named chronic sublimit, but outpatient claims reduce the same annual pool. | How much inpatient cover remains after outpatient use? |

| Waiting periods | Different benefits can have different waiting periods running at the same time. | Which waiting period applies to my condition or benefit? |

| Shared family limits | One family member’s claim can reduce what remains for everyone else. | Is this a shared family pool or a per-person limit? |

| Outpatient access | Some plans become useful for outpatient care sooner than buyers expect. | What is the outpatient waiting period for illness? |

| Maternity structure | “Maternity included” may still leave a large delivery or C-section shortfall. | Is C-section capped separately or included in the shared limit? |

Affordable Health Insurance Plans in Kenya: What Each Plan Really Offers

This section looks beyond price to show what each plan really gives you: the useful benefits, the limits to watch, and the trade-offs that matter at claim time.

1. Madison Betterlife Budget

Best for:

A family that wants broad cover in one plan without managing separate medical, dental, and optical policies.

Amssurity advisory verdict:

A strong all-in-one family option for buyers who want breadth. But do not buy it on the inpatient headline alone. Confirm the chronic, cancer, and specified illness sublimits before paying.

What it covers:

This is one of the broadest covers in this price bracket. It bundles inpatient, outpatient, dental, and optical benefits into one plan, with a family premium of approximately KES 150,000.

Watch carefully:

The headline inpatient limit can be misleading if you do not check the serious illness wording. Cancer and chronic illness claims may sit under a separate sublimit that is much lower than the main inpatient figure.

Before buying, ask for the exact chronic illness and specified illness sublimit. That number matters more than the headline inpatient limit if a serious diagnosis occurs.

Waiting period to know:

Maternity has a 10-month waiting period. If pregnancy is already likely or planned soon, timing matters. This plan needs to be bought before conception, not after a positive test.

Key limits:

- Inpatient: KES 500K–1.5M

- Outpatient: KES 50K–100K

- Maternity: KES 30K–75K: Included inside inpatient

- Dental and optical: Included inside outpatient

2. Britam Bima ya Mwananchi

Best for:

A young, healthy individual or couple buying private medical cover for the first time.

Amssurity advisory verdict:

Good for first-time cover where the alternative is having nothing. Weak for anyone with a known procedure, recurring condition, or likely hospital admission risk.

What it covers:

This is the lowest entry point in the guide, with premiums from approximately KES 4,661 per adult. It works best as a foundation for someone who currently has no cover at all.

Watch carefully:

The minimum inpatient limit of KES 75,000 is thin. A short admission in a mid-tier Nairobi hospital can consume a large part of that limit.

This plan reduces exposure, but it does not create deep protection. Treat it as a starting point, not full medical security.

Waiting period to know:

Elective surgery has a 12-month waiting period. If you already know you may need a planned operation — for example a hernia repair, joint procedure, or scheduled surgery — this plan will not help in the first year.

Key limits:

- Inpatient: KES 75K–500K

- Outpatient: KES 30K–75K

- Maternity: KES 20K–30K

- Premium: From KES 4,661 per adult

3. Old Mutual Afyaimara County

Best for:

Families outside Nairobi or buyers who may need emergency transfer to a specialist hospital.

Amssurity advisory verdict:

A practical mid-range option for upcountry families, especially where emergency transfer is a real concern. But the evacuation benefit should be confirmed tier by tier before relying on it.

What it covers:

The standout feature is air evacuation — a benefit that matters for families living away from major specialist hospitals and that most budget plans in this guide do not include.

Watch carefully:

Air evacuation applies only on the KES 1M inpatient tier. If you choose a lower tier to manage cost, do not assume evacuation is included.

Always confirm the exact tier your premium is buying before relying on this benefit.

Waiting period to know:

Maternity and pre-existing conditions both have a 12-month waiting period. If you have a pre-existing condition and are also planning a family, both clocks start when the policy begins.

Key limits:

- Inpatient: KES 100K–1M

- Outpatient: KES 25K–50K

- Maternity: KES 30K–50K

- Air evacuation: Available on 1M tier only

4. APA Afya Nafuu

Best for:

Families that use outpatient care regularly — doctors, clinics, specialists, tests, and medication.

Amssurity advisory verdict:

Strong for families that actually use outpatient care. Less suitable for buyers who want a fuller all-in-one package with dental and optical included.

What it covers:

This has one of the strongest outpatient structures in the comparison, with outpatient limits of up to KES 100,000 for a family. If your household runs regular outpatient bills, this structure rewards it.

Watch carefully:

There is no dental or optical cover at any tier. This is not a problem if your priority is medical outpatient access, but it matters if you expect dental and optical to be included.

Waiting period to know:

Scheduled surgery has a 90-day waiting period. If you have an operation already planned within the next three months, this plan may not respond.

Key limits:

- Inpatient: KES 100K–1M

- Outpatient: KES 30K–100K

- Maternity: KES 50K–100K

- Dental and optical: Not included

5. Jubilee J-Care Cover Bora

Best for:

A budget-constrained family that wants inpatient protection only and is ready to pay outpatient costs from pocket.

Amssurity advisory verdict:

A clean inpatient safety-net product. Good if the buyer understands exactly what is excluded. Wrong for families that visit doctors regularly.

What it covers:

This plan does one thing: inpatient protection at a very low mainstream premium. Family cover starts from approximately KES 12,600. No medical exam is required. The simplicity is the point.

Watch carefully:

There is no outpatient cover. Not a small outpatient limit. Not a shared outpatient limit. None.

Every GP visit, lab test, specialist consultation, prescription, and outpatient bill is paid out of pocket.

Waiting period to know:

Maternity has a 9-month waiting period. If family planning is near-term, the policy needs to be active before conception.

Key limits:

- Inpatient: KES 250K–500K

- Outpatient: Not included

- Maternity: Included

- Premium: From KES 12,600 per family

6. Jubilee J-Care Johari

Best for:

Buyers who want a simple plan with both inpatient and outpatient benefits at a tight premium level.

Amssurity advisory verdict:

A practical starter plan for buyers who want inpatient and outpatient cover together. But the inpatient limit must be chosen carefully if private hospital access matters.

What it covers:

It offers inpatient and outpatient cover under one simple structure, with no medical exam required. For a buyer stepping off employer cover or starting fresh, it removes the friction of a health declaration.

Watch carefully:

The inpatient ceiling of KES 200,000–400,000 may be thin for a serious private hospital admission. A week in a mid-to-premium Nairobi hospital can exhaust the lower tiers.

Before choosing a limit, check your preferred hospital’s room rate, theatre costs, and admission deposit expectations.

Waiting period to know:

Pre-existing and chronic conditions have a 12-month exclusion. No medical exam makes the plan accessible, but known conditions remain self-funded during the first year.

Key limits:

- Inpatient: KES 200K–400K

- Outpatient: KES 40K–50K

- Maternity: KES 40K–50K

- Medical exam: Not required

7. CIC Afya Bora

Best for:

A large, generally healthy family looking for baseline cover at a very low family premium.

Amssurity advisory verdict:

Good value for large healthy families that need affordable baseline protection. Riskier where one serious claim could exhaust the shared pool before the year ends.

What it covers:

The value-per-member pricing is strong: approximately KES 32,000 flat for up to six people. For a large family where per-head cost matters, this is hard to beat at this price point.

Watch carefully:

All six members draw from the same KES 250,000 inpatient pool. If one person has a serious admission, the shared family limit can reduce quickly for everyone else.

This structure works better for healthy families than for families with chronic conditions or multiple likely claimants.

Waiting period to know:

Pre-existing and chronic conditions have a 6-month waiting period — shorter than most competing options in this guide.

Key limits:

- Inpatient: KES 250K shared

- Outpatient: KES 50K shared

- Pre-existing sublimit: KES 50K inpatient / KES 20K outpatient

- Premium: KES 32,000 flat for up to 6 members

8. AAR ShwAARi

Best for:

A buyer who needs medical cover to start quickly — after leaving employment, between policies, or after a long uninsured period.

Amssurity advisory verdict:

Strong for fast-start protection. Less suitable for buyers whose main concern is maternity, chronic illness, or pre-existing conditions — those benefits do not follow the 7-day waiting period.

What it covers:

The 7-day illness waiting period is unusually short compared to most private medical plans in Kenya. For a buyer who needs cover to start now rather than in 30 or 90 days, this is the clearest option in the guide.

Watch carefully:

Outpatient and inpatient draw from the same annual pool. If you buy a KES 250,000 limit, outpatient is capped at KES 75,000. Every outpatient visit reduces what remains if you are later admitted.

Waiting period to know:

The 7-day wait applies only to general illness. Maternity, pre-existing conditions, and chronic conditions have a 10-month waiting period. Do not assume the 7-day headline applies across the whole policy.

Key limits:

- Single annual limit: KES 250K–1M

- Outpatient: Capped at 30% of annual limit

- Maternity: Included

- Dental and optical: Included

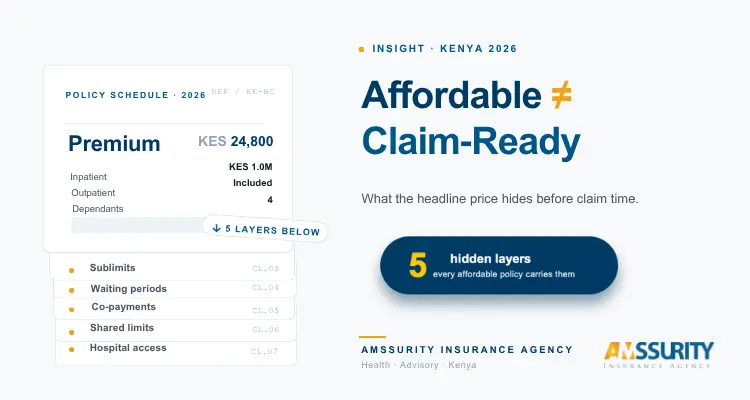

What the brochure does not show clearly

Every plan in this guide tells you what it covers. The harder question is what happens when the benefit runs out, when a lower sublimit applies, or when a waiting period blocks the claim.

These are the six claim-time realities to check before you buy.

The six checks that matter most

| Plan | Best for | Main caution |

|---|---|---|

| Madison Betterlife Budget | Families wanting broad bundled cover | Chronic and cancer claims may sit under a lower sublimit |

| Britam Bima ya Mwananchi | First-time buyers needing low-cost cover | Low inpatient limits can be exhausted quickly |

| Old Mutual Afyaimara County | Families outside Nairobi needing evacuation access | Air evacuation applies only on the 1M tier |

| APA Afya Nafuu | Families with regular outpatient use | No dental or optical cover |

| Jubilee J-Care Cover Bora | Budget buyers wanting inpatient-only protection | No outpatient cover at all |

| Jubilee J-Care Johari | Buyers wanting simple inpatient + outpatient cover | Inpatient ceiling may be thin for serious admissions |

| CIC Afya Bora | Larger healthy families on a tight budget | Shared family pool can deplete quickly |

| AAR ShwAARi | Buyers needing cover to start quickly | Outpatient and inpatient draw from one annual pool |

Reality 1: Your inpatient limit and your chronic illness limit are not always the same figure

Most plans in this guide apply a separate sublimit to chronic conditions, pre-existing conditions, and specified illnesses. This sublimit is usually lower — sometimes significantly lower — than the headline inpatient figure on the brochure.

AAR ShwAARi works differently, which is why it is explained separately below.

On Britam Bima ya Mwananchi, the chronic illness sublimit ranges from KES 37,500 to KES 250,000, depending on the option chosen. On the entry KES 75,000 inpatient plan, the ceiling for a chronic condition claim is KES 37,500.

The plan does not become worthless. But it covers approximately half of what the headline inpatient limit suggests.

On Madison Betterlife Budget, the shared family sublimit for chronic and specified illness ranges from KES 150,000 to KES 300,000, against a headline inpatient figure of up to KES 1.5M.

If the family sublimit on your tier is KES 150,000, your effective cancer or chronic illness cover is one-tenth of the plan’s stated inpatient ceiling.

Before buying:

Ask for the chronic illness, specified illness, and pre-existing condition sublimit in writing. It is usually in the benefit schedule, not the headline brochure.

Reality 2: AAR works differently — and that matters for serious illness

AAR ShwAARi does not apply a named chronic illness or pre-existing condition sublimit.

Once through the 10-month inpatient waiting period, chronic and cancer claims may draw from the shared annual pool without a separate named ceiling, reducing the cover.

This is structurally more generous for serious illness.

But the risk changes.

On a KES 250,000 plan, outpatient use is capped at KES 75,000, which is 30% of the annual limit. Every outpatient claim reduces what remains for inpatient care.

If you use KES 75,000 in outpatient care before a serious admission, your effective inpatient balance is KES 175,000, not the full KES 250,000 headline.

The risk is not a named chronic illness sublimit. It is sequential pool depletion.

Know which risk you are managing before choosing this plan.

Reality 3: Two waiting periods can run at the same time

On Old Mutual Afyaimara County, a pre-existing condition carries a 12-month inpatient waiting period. A newly diagnosed condition may carry a shorter waiting period of 28 to 60 days, depending on the condition and schedule wording.

That distinction matters, especially for serious illness.

A condition diagnosed after the policy starts may be treated differently from a condition that existed before the policy began. That can change which waiting period applies.

If maternity is also relevant, the maternity waiting period runs from the same policy start date. Both clocks run from the policy start date. Every month you delay buying reduces what is available when you need it.

Before buying:

Ask which waiting period applies to your specific situation: pre-existing, newly diagnosed illness, maternity, surgery, or outpatient treatment.

Reality 4: CIC Afya Bora applies a sublimit inside a shared family pool

CIC Afya Bora operates on a shared family inpatient pool of KES 250,000.

Pre-existing and chronic conditions carry an additional sublimit of KES 50,000 within that pool.

For a family of six, this creates two layers of compression:

the chronic condition ceiling is KES 50,000, and that amount is drawn from a pool serving the whole family.

If more than one family member has a chronic condition claim, those claims draw from the same KES 50,000 ceiling.

The flat KES 32,000 family premium is genuine value for a healthy family with no chronic conditions.

For a family where one member is already managing an ongoing condition, the key issue is different: a sublimit inside a shared pool.

That structure should be understood before buying.

Reality 5: “Maternity included” is not the same as maternity covered in full

Most plans in this guide include maternity benefits.

But maternity cover depends on two things:

whether the plan gives maternity a named sublimit or includes it in a shared inpatient limit, and the actual cost of delivery at the hospital you plan to use.

Those two details decide the out-of-pocket gap.

What mid-tier Nairobi hospitals currently charge

A normal delivery at Nairobi Women’s Hospital ranges from approximately KES 30,000 to KES 64,000, depending on the package.

At Nairobi West Hospital, a normal delivery costs approximately KES 55,000 to KES 130,000.

At Coptic Hospital, the range is approximately KES 55,000 to KES 80,000.

A C-section changes the calculation.

Nairobi Women’s Hospital charges approximately KES 145,000. Coptic Hospital charges approximately KES 185,000 for an elective C-section and KES 195,000 for an emergency C-section. Nairobi West Hospital charges approximately KES 168,000 to KES 318,000, depending on procedure and ward level.

Where the gaps appear

Britam Bima ya Mwananchi pays a flat KES 45,000 for a C-section.

That may be adequate at a lower-cost maternity facility such as Jacaranda Maternity Hospital, where a C-section costs approximately KES 41,000 to KES 55,000.

It is not enough for many mid-tier private Nairobi hospitals.

At Nairobi Women’s Hospital, the shortfall is approximately KES 100,000. At Coptic Hospital, the shortfall is approximately KES 140,000. At the upper range of Nairobi West Hospital, the shortfall can be approximately KES 273,000.

For plans where C-section is included in the shared inpatient limit — including Madison, APA, Old Mutual, CIC, Jubilee CoverBora, and Jubilee Johari — the full C-section cost draws from the main inpatient pool.

That can create a different problem.

On a CIC Afya Bora plan with a shared family pool of KES 250,000, a C-section at Coptic costing KES 185,000 would consume about 74% of the entire family’s inpatient cover for the year.

Every other admission for every other family member would then draw from what remains.

Before buying for maternity, do three things

- First, call the hospital where you plan to deliver. Ask for the current normal delivery and elective C-section package costs. Prices vary by ward level and can change.

- Second, check whether C-section has a named benefit limit or is included in the shared inpatient limit.

- Third, calculate the difference between the hospital cost and the maternity benefit on the tier you are buying.

That difference is the amount you should be ready to pay out of pocket.

Important note before you buy

Maternity hospital costs are based on publicly available hospital pricing reviewed in May 2026. Plan benefit data is based on insurer benefit schedules reviewed in May 2026.

Benefits, sublimits, waiting periods, hospital costs, and premiums can change.

Before buying or renewing cover, confirm the current benefit schedule with the insurer or your broker.

Before you call a plan affordable: a 30-second checklist

A low premium is not enough. Before choosing any affordable medical insurance plan in Kenya, check the real claim-time details.

- Limits: Check inpatient, outpatient, maternity, chronic illness, cancer, and pre-existing condition sublimits.

- Waiting periods: Confirm maternity, chronic illness, surgery, outpatient illness, and pre-existing condition waits.

- Hospital panel: Make sure your preferred hospitals and clinics are included.

- Copayments: Ask what you pay per visit, admission, or procedure.

- Age bands: Check how the premium changes as you or your dependants move into older brackets.

The test: affordable cover should lower your claim-time risk, not just your annual premium.

AMSSURITY INSURANCE AGENCY

FAQs about affordable health insurance in Kenya

Short answers to the common questions buyers ask before choosing a low-cost medical cover.

How much does affordable health insurance cost in Kenya?

Affordable health insurance can start from about KSh 12,600 per year for basic inpatient-only family cover and rise toward KSh 135,000–150,000 depending on age, benefits, and hospital access.

Which is the most affordable health insurance in Kenya?

It depends on what you mean by affordable. Jubilee Cover Bora is strong on low premiums, AAR Shwaari may suit shorter waiting periods, APA Afya Nafuu is a strong budget option, and Madison Betterlife may suit hospital-selection needs.

Is SHA enough on its own?

SHA is an important baseline, but many families still need private cover for wider hospital choice, outpatient access, specialist care, maternity planning, or higher claim flexibility.

Which insurance company in Kenya accepts seniors over 65?

Some insurers accept seniors above 65, but rules vary by plan, entry age, renewal age, underwriting, and pre-existing conditions. Confirm the latest schedule before applying.

Can I customise affordable health insurance?

Yes. Many insurers let you start with inpatient cover and add outpatient, maternity, dental, optical, or last-expense benefits. Keep only what fits your real risk.

Do low-cost plans cover chronic conditions like diabetes or hypertension?

Some do, but usually with waiting periods, sublimits, exclusions, or medical underwriting. Ask clearly: Is it covered? From when? Up to what limit? Under which benefit?

Need help choosing affordable health insurance in Kenya?

No single affordable health insurance plan suits everyone. Your budget, hospital preference, family size, health history, maternity plans, and outpatient needs should guide the choice — not just the lowest premium.

Amssurity helps you compare suitable options side by side, understand the sublimits and waiting periods, and spot claim-time gaps before you buy.

The cheapest cover is only useful if it still works when you need it.

Source basis:

This guide is based on publicly available insurer benefit summaries, policy schedules, product brochures, hospital-access information, and Amssurity’s advisory review of affordable retail medical insurance options in Kenya.

Where benefit limits, waiting periods, maternity caps, chronic illness sublimits, co-payments, or hospital-panel rules are mentioned, treat them as decision points to confirm before buying. Insurers can update benefits, premiums, hospital panels, and underwriting rules.

Last reviewed: June 2026. Before paying for any plan, ask for the latest official benefit schedule and confirm the specific terms that apply to your age, dependents, medical history, preferred hospitals, and budget.

Agnes Mukulu is the Principal Broker and Founder of Amssurity Insurance Agency, an IRA-licensed independent insurance agent based in Nairobi.

She helps individuals, families, and SMEs compare cover beyond the premium — with specific attention to sublimits, waiting periods, hospital access, and claim-time gaps.”

Her work focuses on helping buyers choose cover they understand before they pay for it.